Despite elevated interest rates, concerns over sticky inflation, geopolitical uncertainty, and pricy valuations, the S&P 500 has continued to push toward new highs, closing the second quarter up 10.2% year-to-date.[1] Understandably, many investors are asking whether the market has gotten ahead of itself.

It seems the recent rally has been supported by something more durable than investor optimism. It's been exceptional corporate profitability. It's worth understanding what's actually driving that trend.

Earnings Growth: A Historic Run

According to FactSet’s most recent Earnings Insight (June 26, 2026), the S&P 500 is on track to report year-over-year earnings growth of 23.1% for the second quarter of 2026.[2] If that holds, it will be the second consecutive quarter of earnings growth above 20% and the seventh straight quarter of double-digit growth. For context, this is well above both the five-year average earnings growth rate is 16.4% and the ten-year average is just 10.3%.

Equally notable: analysts have been raising estimates during the quarter, not cutting them. Historically, estimates fall roughly 2–3% through a quarter as caution sets in. This quarter, they have risen by 3.4% since March 31, when the consensus stood at 18.8%. That kind of positive revision is unusual and reflects genuine earnings momentum.

Elevated Valuations—and Why They May Be Justified

With markets having rallied sharply, price-to-earnings ratios are elevated relative to historical norms. This is a legitimate concern worth acknowledging. However, high valuations are more defensible when earnings growth is this robust.

The forward picture supports this view. Analysts project full-year 2026 earnings growth of 24.0% and further growth of 16.8% in 2027. The forward 12-month P/E ratio of 20.1 is above both the 5-year average of 19.9 and the 10-year average of 19.0—elevated, but not dramatically so given the earnings trajectory. If those estimates prove reasonable, much of today’s premium compresses naturally as earnings rise to meet current prices. That is a very different situation from a bubble built on hope rather than results.

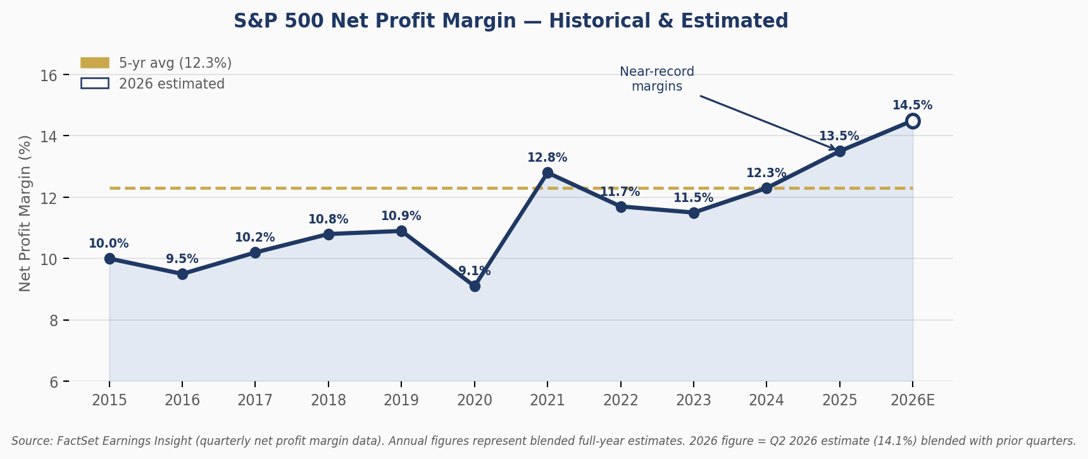

Profit Margins at Record Levels

A key reason for this growth is improving profit margins. The estimated net profit margin for the S&P 500 in Q2 2026 is 14.2%—which would be the second-highest on record since FactSet began tracking this figure in 2009.[3] The only quarter to exceed it was Q1 2026 at 14.8%. The five-year average is 12.3%. Companies are growing revenues and keeping more of each dollar as profit.

Figure 1: S&P 500 Net Profit Margin, 2015–2026E. Sources: FactSet Earnings Insight (quarterly reports). 2026 reflects Q2 2026 estimate blended with prior quarters.

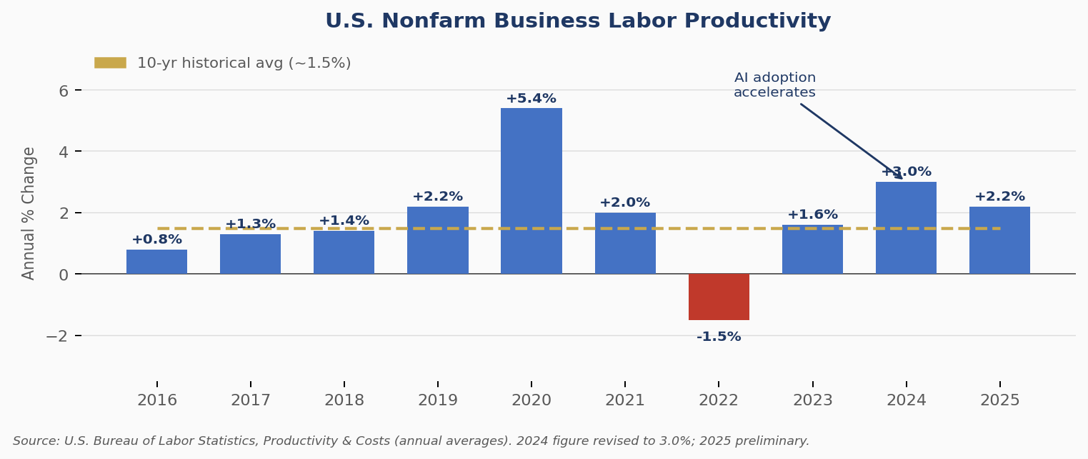

It is worth pausing to ask what is actually driving these record margins. Revenues are growing at 12.3%, but earnings are growing at 23.1%. That gap has to come from somewhere, and it is coming from labor—the one cost that has not kept pace with output.

The productivity data reinforces this point. U.S. nonfarm business labor productivity grew 3.0% in 2024 and 2.2% in 2025—both well above the ten-year historical average of roughly 1.5%.[4][5] Output is expanding faster than hours worked as evidenced by the chart below.

Figure 2: U.S. Nonfarm Business Labor Productivity, Annual % Change, 2016–2025. Source: U.S. Bureau of Labor Statistics, Productivity & Costs.

Critically, this margin story has so far been concentrated in technology. Apollo’s chief economist published analysis earlier this year showing that over the past 20 years, essentially all of the increase in the S&P 500’s operating margin has come from tech-related sectors, while operating margins for the rest of the index have stayed near 9%—roughly flat for two decades.[6] Strip out technology, and the headline margin picture looks considerably more ordinary.

The Next Phase: AI Broadening Beyond Tech

The question worth asking now is whether these gains will spread beyond technology. The early evidence says yes, though unevenly: adoption is already broad, but measurable financial payoff is still concentrated in a narrower set of use cases and companies. On the adoption side, roughly 37% of U.S. companies with 250 or more employees now use AI in their operations, and more than 40% of American workers report using generative AI on the job[7]—adoption that has happened in roughly three years. In financial services, JPMorgan puts the value from AI at roughly $1.5 billion, spanning fraud detection, trading, and back-office efficiency.[8] A March 2026 NBER study of nearly 750 executives confirms positive productivity gains across sectors, with the strongest near-term effects in services and finance.[9]

That said, a PwC survey found 56% of CEOs have yet to see measurable revenue or cost impact from their AI investments.[10] BlackRock’s equity team describes the list of companies with tangible AI-driven margin improvement as “small but growing.”[11] Goldman Sachs estimates AI could add roughly 1.5 percentage points to annual U.S. productivity growth over the next decade.[12] If non-tech margins move even modestly off their long-standing 9% floor, the companies leading that shift will be worth owning.

Portfolio Positioning

As this AI led productivity trend plays out, we remain constructive on equities and have maintained meaningful exposure to large-cap growth and technology. At the same time, we are watching closely for evidence of AI-driven margin improvement spreading into non-tech sectors. The speed of the recent rally warrants discipline on valuation, and we continue to monitor macroeconomic risks that could disrupt the earnings trajectory.

Advisory services offered through APG Capital Asset Management, a Member of Advisory Services Network, LLC. All views/opinions expressed are solely those of the author and do not reflect the views/opinions held by Advisory Services Network, LLC. The information herein is of a general nature and is intended for educational purposes only. This material does not constitute a recommendation or solicitation for the purchase or sale of securities. Past performance does not guarantee future results. See footnotes for full source citations.

[1]S&P 500 total return of 10.2% year-to-date through market close on June 30, 2026 (price return of 9.6%, dividend return of 0.7%). Source: S&P Dow Jones Indices data, as compiled by Slickcharts, "S&P 500 Year to Date Return." https://www.slickcharts.com/sp500/returns/ytd

[2]FactSet, "Earnings Insight," June 26, 2026. https://advantage.factset.com/hubfs/Website/Resources%20Section/Research%20Desk/Earnings%20Insight/EarningsInsight_062626.pdf

[3]FactSet Earnings Insight, June 26, 2026: Q2 2026 estimated net profit margin 14.2%, second-highest on record since 2009. Record was 14.8% in Q1 2026. Five-year average: 12.3%. IT sector estimated margin: 30.7% vs. 5-year average of 25.3%.

[4]U.S. Bureau of Labor Statistics, "Productivity and Costs — Annual Averages 2025, Revised," March 5, 2026. https://www.bls.gov/news.release/archives/prod2_03052026.htm

[5]U.S. Bureau of Labor Statistics, "Productivity up 2.3 percent in 2024," The Economics Daily, February 12, 2025. https://www.bls.gov/opub/ted/2025/productivity-up-2-3-percent-in-2024.htm

[6]Torsten Sløk, Apollo Chief Economist, "S&P 500 Margin Expansion All Coming from Tech," Apollo Academy, January 25, 2026. https://www.apolloacademy.com/sp-500-margin-expansion-all-coming-from-tech/

[7]Commonfund, "AI’s Productivity Payoff Is Here," June 18, 2026. https://www.commonfund.org/blog/ais-productivity-payoff-is-here

[8]JPMorgan Chase management commentary, Q4 2025 earnings call; cited in Investing.com, "JPMorgan Chase AI Spending Targets Cost Savings and Margin Gains," April 8, 2026. https://www.investing.com/analysis/jpmorgan-chase-ai-spending-targets-cost-savings-and-margin-gains-200678084

[9]Baslandze et al., "Artificial Intelligence, Productivity, and the Workforce: Evidence from Corporate Executives," NBER Working Paper 34984, March 2026. https://www.nber.org/papers/w34984

[10]PwC CEO Survey 2026, cited in Svitla Systems, "AI ROI and Cost Optimization in 2026," May 2026. https://svitla.com/blog/ai-roi-and-cost-optimization-in-2026/

[11]BlackRock Fundamental Equities, "Choosing Stocks Outside the Magnificent 7," February 2026. https://www.blackrock.com/us/individual/insights/stock-investing-outside-the-magnificent-seven

[12]Goldman Sachs Research, cited in Commonfund, "AI’s Productivity Payoff Is Here," June 18, 2026. Goldman estimates generative AI could lift U.S. productivity by ~1.5 percentage points annually over the coming decade.